Author:Wall Street CN

The global markets are currently experiencing an unusually high-noise, high-flow period, with a level of chaos that is perplexing even to the most seasoned traders. Tony Pasquariello, head of hedge fund operations at Goldman Sachs, bluntly stated that aside from major traumatic periods such as the global financial crisis or the COVID-19 pandemic, it's difficult to recall a time when the market environment has been so "extremely open" and unpredictable. In his latest report, he warned: no one really knows how this will end.

The market's core anxiety stems from the fierce competition between two diametrically opposed AI narratives:On the one hand, the market believes that the disruptive risks brought about by artificial intelligence are prolonging, which has led to a sharp sell-off in the "victims" sector; on the other hand, investors have begun to question whether the return on AI capital expenditures is ideal enough.This inherent tension leads to dramatic fluctuations—sell-offs become exceptionally fierce as soon as the market perceives marginal AI risks.

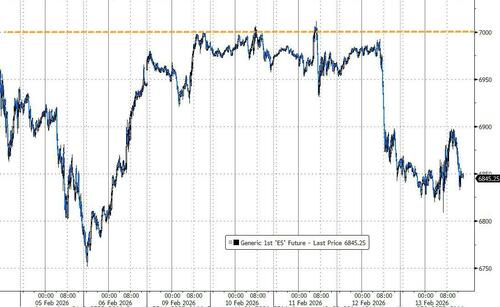

The S&P 500 has stalled at the 7,000-point mark this year, failing to break through, and beneath the calm surface, undercurrents are stirring. Goldman Sachs' "AI Leaders vs. Laggards" pairing trade saw its largest single-day gain in history last week, but this was primarily driven by shorting the "laggards." This "fire first, aim later" short-selling sentiment is causing dramatic narrative fluctuations and risk shifts in core sectors such as software.

Meanwhile, due to overcrowding and valuation pressures in the US stock market, global capital allocation is undergoing a subtle but significant shift. As the narrative in the US domestic market becomes more complex, incremental funds are accelerating their flow overseas. South Korean and Japanese stock markets have recently performed strongly, particularly the South Korean KOSPI index, which, driven by the "Corporate Value Enhancement Plan" and strong earnings expectations, has not only doubled since the end of 2024 but also recently recorded its best weekly performance in five years, indicating that investors are seeking new growth safe havens in non-US markets.

Confusing signals: An extremely difficult trading environment

The current market environment is filled with conflicting signals, making investment extremely challenging. Tony Pasquariello points out that the market is simultaneously buying cyclical assets (such as industrial stocks and raw materials) and defensive assets (such as consumer staples and utilities), a phenomenon that is extremely rare.

A similar contradiction also exists between the commodities and interest rate markets:The surge in demand for commodities such as metals suggests a strong economy; however, lower U.S. interest rates and a flattening yield curve are typically signals of an economic slowdown.Goldman Sachs technology expert Pete Callahan believes that this potential volatility and mixed signals make it exceptionally difficult to determine the market’s true sentiment and what narratives are about to shift.

The Battle of AI Narratives: Value Creation and Value Destruction

The current market debate focuses on the fundamental impact of AI: who will benefit and who will be the victim? Will it create or destroy value? Will it be asset-light or asset-heavy? This heated debate has directly led to a surge in the actual volatility of related stocks and thematic baskets.

As the "epicenter" of the market narrative, the software industry is particularly noteworthy. Although the index level appears calm, beneath the surface, the punishment for AI "laggards" is ruthless.As more and more sub-sectors come under scrutiny, market participants are increasingly concerned about the disruptive risks of AI.

Furthermore, with the advancement of AI infrastructure construction, electricity demand has become a new and complex variable. Goldman Sachs research points out that the pressure that AI is putting on the power grid is translating into concrete macroeconomic spillover effects, which is also causing a clear pressure signal to the basket of stocks related to the transformation of the US power grid.

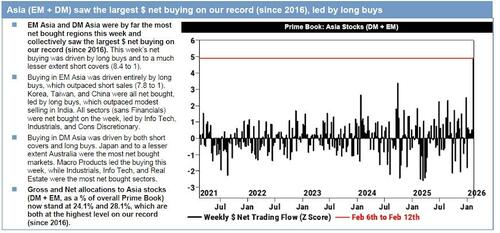

Reversal of Fund Flows: Stagnant US Stocks and Booming Asian Markets

While US stocks failed to break through key resistance levels after the release of non-farm payroll and CPI data, overseas markets experienced a surge. Data from Goldman Sachs strategist Ryan Hammond shows that...This year, non-US equity funds have seen inflows of $89 billion, while US equity funds have only seen $16 billion. This does not mean that investors are directly selling US stocks, but rather that marginal incremental funds are preferentially flowing to non-US markets.

South Korean stocks have become the leader in this trend. The MSCI Korea Index has risen 28% year-to-date in dollar terms. Tim Moe, chief equity strategist for Asia Pacific at Goldman Sachs, maintained his overweight rating and raised his target for the KOSPI index to 6,400 points. He gave four reasons: first, impressive earnings growth, projected to grow 120% in 2026 after a 36% increase in 2025; second, highly attractive valuations, with forward P/E ratios still below the long-term average; third, low foreign ownership; and fourth, substantial progress in corporate governance reforms.

The Japanese market has also performed well, with the Nikkei index rising 5% recently. It's worth noting that the correlation between the Japanese stock market and exchange rate seems to have reversed: previously, a weak yen meant a strong stock market, while now the pattern is a strong yen, low interest rates, yet the stock market still rises. This suggests that the Japanese market may be shifting from a "currency devaluation trade" to a healthier "reflation trade."

Hedge Fund Resilience and Outlook

Despite the uncertain macroeconomic environment, hedge funds have demonstrated remarkable resilience. According to Tony Pasquariello, macro discretionary funds accumulated significant profit buffers in January, while equity long-short strategies (whether fundamental or quantitative) generally mitigated risk.

Looking ahead, market trends appear to favor active management over passive investing, and highly liquid assets over illiquid assets. In this noisy and fast-moving market, strategies that can flexibly adapt to changing narratives seem to be gaining the upper hand.